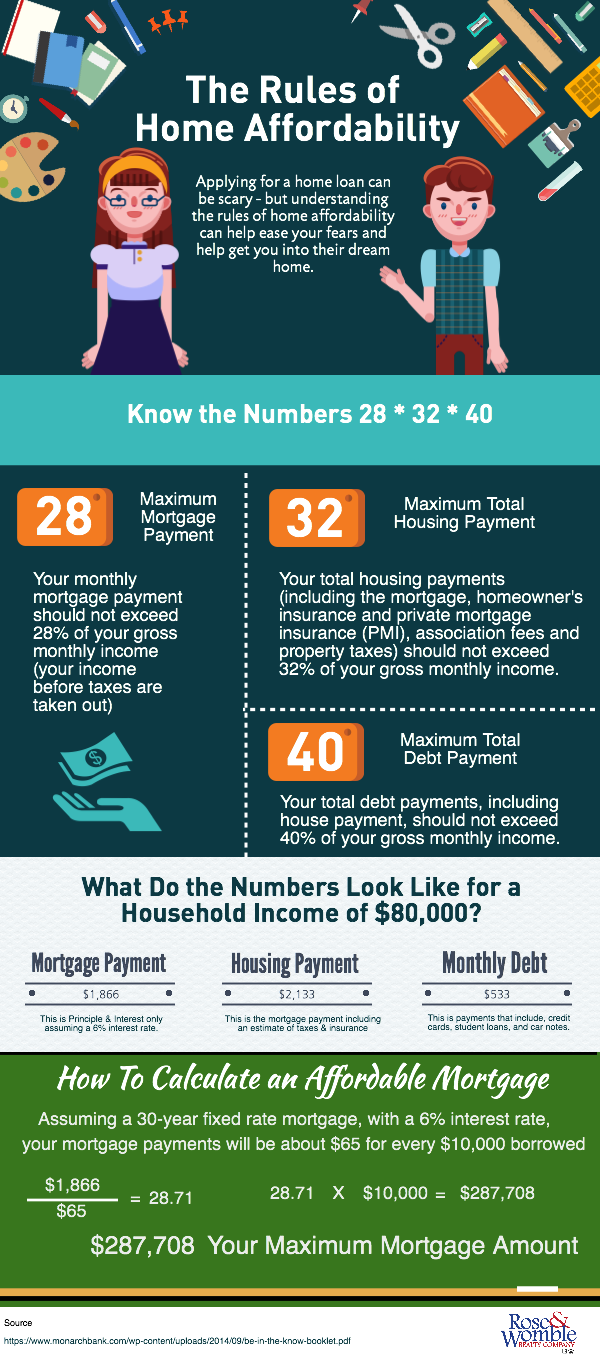

Applying for a home loan can be scary – but understanding the rules of home affordability can help ease your fears and help get you into your dream home. The key is to understand the rules of home affordability. Our great relationship with Advance Financial Group, a division of Monarch Mortgage, allows us to get some great insight and information about qualification ratios that help mortgage lenders determine how much they will lend to a home buyer. Each lender has its own set of ratios, but majority fall under these limits.

Home buyers must understand the rules of 28, 32, and 40.

Rule of 28% is the maximum mortgage payment a responsible lender will allow you to take on. The mortgage payment is a combination of principal and interest and it cannot exceed 28% of your gross monthly income. Gross monthly income is your pay before taxes are taken out.

Rule of 32% is the maximum total housing payment a responsible lender will allow you to have. This will include the mortgage payment, homeowner’s and private mortgage insurance (PMI), association fees, and property taxes. The number should not be more that 32% of your gross monthly income.

Rule of 40% is the maximum debt payments you currently have. This will include your housing payment, auto and student loan payments, and minimum credit card payments. These items should not exceed 40% of your gross monthly income.

For specific answers for your mortgage questions, we recommend visiting Advance Financial Group’s website. They have great tools and currently information about rates and home buyers programs.